")

Good old paper checks have been around since 1681, when the first was recorded in the U.S. But if we really want to go back to the origins of payments, merchants in Mesopotamia were using clay tablets as promissory notes around 3000 BC.

Some people hear that and think, “Wow. A payment method that’s lasted 5,000 years must be doing something right.”

If it was good enough for Mesopotamian merchants five millennia ago, surely it’s good enough for us… right?

Well, so were manual ledgers, clay tablets, and waiting weeks for confirmation.

The truth of the matter is, paper payments weren’t adopted because they were brilliant. They were adopted because there wasn’t a better option yet. No automation. No real-time data. No fraud protection. Just the best tool available at the time.

Fast-forward a few thousand years and we have better tools.

At ePayPolicy, our team (and 10,000+ insurance organizations) think it’s time we stop treating checks like a sacred tradition.

But hey, we also get it– paper checks feel familiar. Safe. “Good enough.”

Unfortunately, that’s simply not the case. In fact, check fraud has increased every year since 2021, with 80% of companies reporting incidents. One security breach or compliance violation can wipe out years of perceived “savings”—plus leave behind reputational damage that doesn’t just disappear.

Across insurance and B2B payments as a whole, manual payment processes drive a whopping $32 billion in preventable losses every year. And most organizations don’t even notice it happening. Every check processed, every envelope mailed, every manual reconciliation (death by a thousand paper cuts).

The good news? This problem has a clear solution, and doesn’t involve spending more money to fix it. It’s actually about eliminating losses you’re already absorbing.

You see, digital payments don’t just replace paper. They accelerate cash flow, slash errors, and close compliance gaps that quietly limit growth.

Paper had a great run. It’s just not built for modern insurance.

The Hidden Financial Drain of Manual Payments

In the insurance world, paper checks are often viewed as a “fixed cost of doing business.” Because the expenses are spread across different departments (postage in one bucket, labor in another, bank fees in a third), the true total is rarely consolidated.

You might see the $.50 bank fee and not bat an eye, but it’s the $4-$20 processing fee that sneaks up on insurance organizations.

1. The Cost of Doing Nothing = Lost Capital

Manual payments are expensive even before something goes wrong. When the “soft costs” are finally brought into the light, the math isn’t something that can be ignored.

- The Invisible Process Tax: You aren’t just paying for a stamp; you’re financing an obsolete, linear workflow. Every time a check changes hands, your margin shrinks.

- The Math: Processing 500 checks a month? That’s $120,000 a year in operational burn.

- The Interest-Free Loan: On $50M in annual premiums, a 5-day mail/processing lag locks up $685,000 in unproductive working capital.

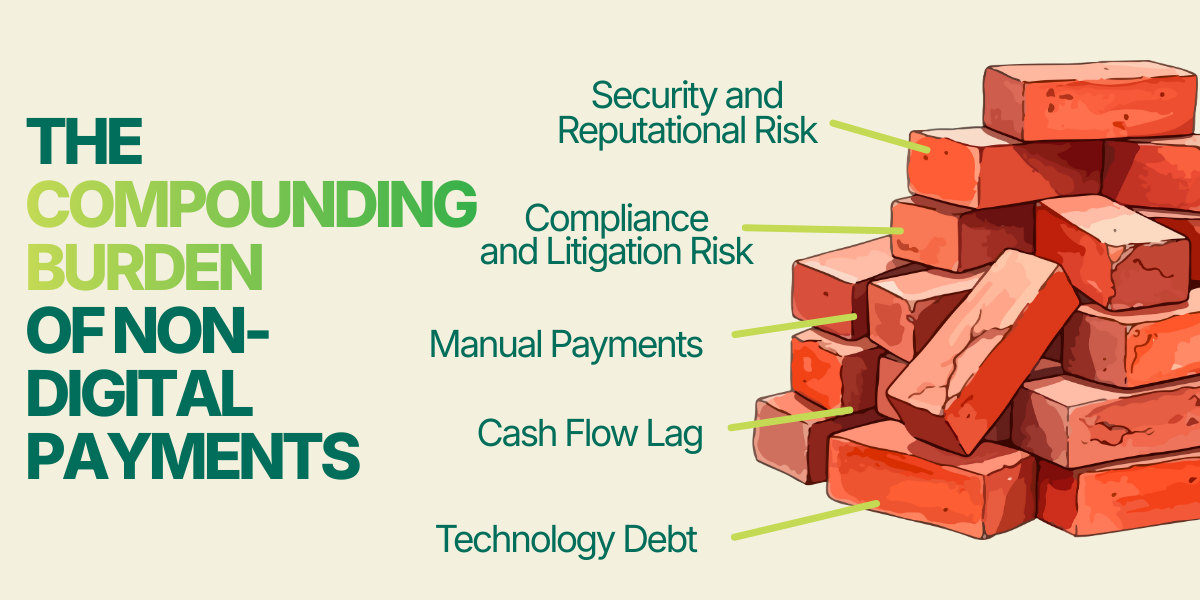

2. The Risk That Compounds Over Time

As an insurance leader, you’re in the business of managing risk. Yet, the way most businesses handle payments is a liability in itself.

Relying on manual workflows and paper checks does more than just slow you down; it creates a threat to your growth and security.

Beyond the slow cash flow and manual grind, sticking with the status quo introduces three critical risks to your organization’s profitability and security:

- Technology Debt: Simply put: manual processes don’t scale. Growth requires more headcount, locking your business into an expensive, linear-cost model.

- Compliance + Litigation Risk: Manually handling sensitive payment data is a litigation time bomb.

- Security + Reputational Risk: The true cost of paper checks lies in the risk they carry. Check fraud has risen every year since 2021, with 80% of recently surveyed companies reporting incidents. The expense of just one security breach or compliance violation will far outweigh more than a decade of supposed “savings,” plus irreparable reputational damage.

Compounded together, this cumulative weight on your organization builds over time until you’re losing thousands or hundreds of thousands to a friction-filled process that should be working for you, not against you.

Where Insurance Leaders Secure 5–6 Figures in Savings

You could be reading this as part of a company who accepts a majority of your premium payments via check. You could also be like some of the insurance leaders we talk to who already have digital payments already in place– but hang on! You’re not off the hook just yet. Even organizations who already have digital payments implemented are often leaving hundreds of thousands of dollars on the table each year, without realizing it’s quietly going down the payments drain.

So the issue isn’t just whether payments are digital; it’s how they’re managed.

The Three Levers That Unlock Real ROI

The organizations that tap into savings from payments aren’t doing it through one dramatic change; they do it by addressing three structural inefficiencies that compound over time.

The first lever is transaction fees. We all hate to see them coming. Though, many insurance organizations absorb card fees as a cost of doing business, even when the premiums are high and payment volume is consistent. At 1.5% – 3.5% per transaction, those fees add up fast, especially for agencies, carriers, and MGAs processing millions of dollars each year.

The fix? Transparently pass service fees to the customer. For high-volume organizations, this can translate into hundreds of thousands of dollars in recouped costs, without sacrificing customer experience or compliance.

The second lever is manual labor. Despite modern payment tools, many teams still rely on people to translate data between systems. You know the drill: logging into portals, copying transaction details, and reconciling payments across AMS platforms– and don’t even get me started on the chaos that ensues from data entry typos. One tiny mistake can set off a domino effect of misapplied payments, broken reconciliations, and hours of rework to fix the error.

But when manual payments are directly integrated with insurance systems, those manual steps become non-existent (because they’re now a non-issue). It’s a beautifully orchestrated symphony: transactions sync automatically, records stay aligned, and staff time is freed up. Think about it: eliminating just 10 hours of manual work per week can translate into more than $25,000 in annual savings– and that number grows as payment volume and team size increase.

The third lever is insurance-specific automation. Generic payment processors are not designed to support the complexity of the insurance ecosystem. Premium allocation, compliance requirements, and audit documentation commonly require manual workarounds that slow teams down and increase exposure. As time goes on, that complexity becomes expensive.

Payments built specifically for insurance means no more workarounds needed. Allocations are handled correctly, compliance becomes a natural part of the workflow, and audit readiness becomes automatic vs reactive.

Together these three levers both reduce cost and fundamentally change how payments support overall business.

The ePayPolicy Difference: A Profit-Generating Investment

We’ve spent a lot of time unpacking where real ROI lives in insurance payments and how leaders can unlock it. So now let’s talk about the vehicle that gets you there: ePayPolicy (we know, the headline of this section may have given this one away).

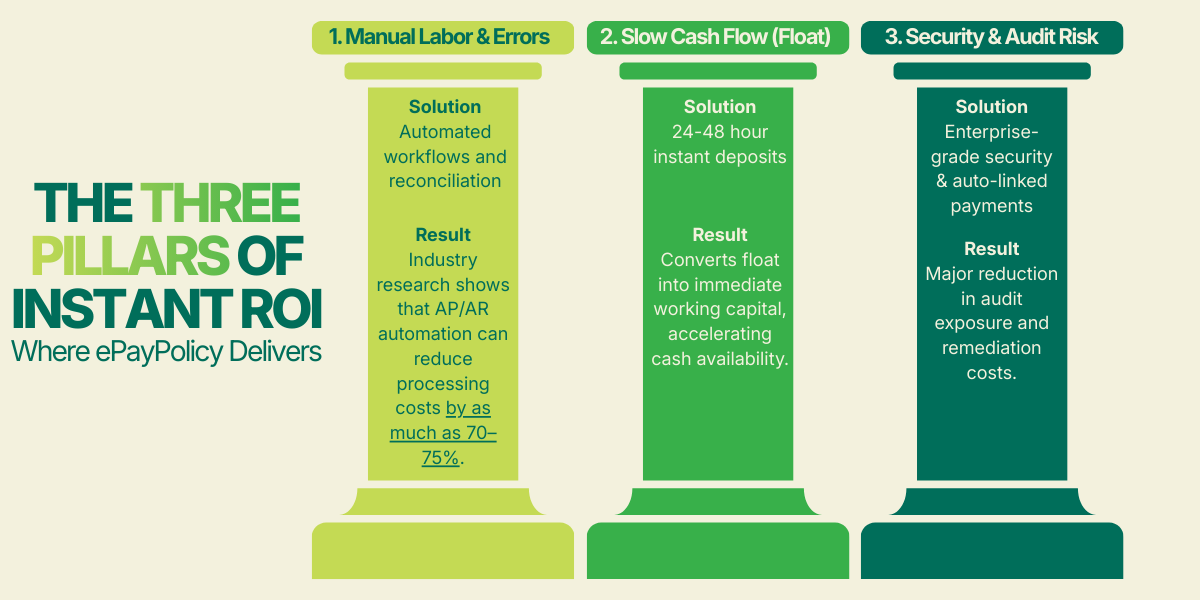

With ePayPolicy, we’ve summed up the way organizations see immediate value in three ways:

First, operational pain gives way to automated workflows. Manual posting, reconciliation, and exception handling are replaced with end-to-end automation that connects payments directly to your insurance systems. Industry research shows that AP and AR automation can reduce processing costs by 70–75%, and for insurance teams, that often translates into fewer handoffs, fewer errors, and more time spent on work that actually moves the business forward.

In fact, one of ePayPolicy’s high-volume customers has achieved an extraordinary operational expense reduction of six-figures per month in through comprehensive workflow digitization. This exemplifies how hidden operational costs often turn into realized savings in as little as 30-90 days.

(Note: Individual savings will vary based on factors like payment volume and existing processes.)

Second, slow cash flow turns into fast, predictable deposits.

Instead of waiting days for funds to clear and reconcile, payments settle in as little as 24–48 hours. By cutting down the time it takes for payments to clear, you turn ‘waiting’ time into available cash. This gives your finance team a real-time view of your bank balance and more confidence in your daily budget.

Third, security and audit risk are replaced with enterprise-grade compliance.

Payments are automatically linked to policies, customers, and documentation, creating a clean, defensible audit trail. That means fewer gaps to explain, less remediation work, and lower exposure in one of the most heavily regulated industries.

So you see, with the right payments foundation in place, organizations came more from constantly managing friction caused by their existing systems and spend their time expanding into new markets and elevating their policy holder experience– all while cash flow is on auto-pilot in the background.

A short review of your current payment volumes and workflows can quickly reveal where savings are hiding and what’s possible with the right approach.

Schedule a consultation with a Payments Specialist to see your personalized savings potential. Your future cash flow will thank you.